Current market uncertainty and volatility make stable income provision over the short-term extremely difficult, although there are definite growth opportunities in the market, these opportunities are likely to unfold over the medium and long-term but with a high degree of market movement in the short-term which is not suitable for consistent short-term income provision.

Current Interest Rates on Money Markets are between 3 to 5.5% +/-. This means the risk free / low risk return rate is now 3% lower than what it was at the beginning of 2020. Thus, it would be unrealistic to expect interest bearing investments to provide the same returns that they have in the past.

Bond yields and thus guaranteed investment rates have risen lately making these types of investments more attractive than they have been over the last few years especially now relative to the super low interest rates.

There are 2 strategies that can be used to counter this low interest rate environment when planning for income provision:

- Take on more risk. Typically, by increasing exposure to growth assets in your retirement portfolios. Since the economic outlook for South Africa is depressed my preferred asset class is offshore equity. There are 2 challenges with this approach.

- Investment regulation on retirement products limit the amount of exposure to growth assets (Equity and Property) and places an additional limitation on offshore assets of 30%. (Reg28)

- Secondly although medium to long-term growth is increased by including Offshore equity it also introduces a high degree of volatility which is not ideal in an income portfolio. So even if your income is provided by an investment that is not subject to Reg 28 you would not want a lot of volatility on an investment that provides a regular income.

- The second option is to Sacrifice Liquidity / Access to Capital in exchange for a Guaranteed Income stream at a rate better than the current risk-free rate (Money Market). This can be done by making use of a Compulsory Life Annuity OR a Voluntary Life Annuity.

The 2 options are discussed below and compared.

Features of Guaranteed Life Annuities (Both Voluntary and Compulsory):

The main feature of any life annuity is that you exchange a capital amount for a guaranteed lifelong income steam. Another way you can think about it is, that “you have bought an income for life” thus the capital is no longer yours, but you do have a right to a risk free income for life. The income you receive for the capital you invest is normally determined by 3 things:

- Your Age, the older you are when you make the investment, the higher your monthly income will be because your life expectancy is shorter thus income is expected to be provided for a shorter period, resulting in higher monthly income payments.

- Your Gender, the fact of whether you are a man, or a woman makes a difference on your life expectancy and thus also affects the expected term for which the income will be provided. This means that for a man and a woman of exactly the same age making the investment on the same day the income paid to the woman will be lower than the income paid to the man. This is because statistically speaking woman live longer than men on average.

- Interest rates, specifically bond rates since these are the underlying investments a provider uses to supply the income in these portfolios, for this reason quotes tend to differ and are only valid from one week to the next week. This is because it depends on what bonds the provider was able to access that week. This for example is why guaranteed rates on these types of investments spiked to 11% & 12% during March 2020 when our bond Yields spiked due to the Credit Downgrade, Oil Price and the Covid Pandemic all hitting at once. Rates still remain attractive especially relative to the extremely low interest rates on cash at the moment.

You have the following options available to you when making your investment in a Guaranteed Life Annuity:

- Number of lives linked to the investment. An annuity can be a Single Life or a Joint Life (2 Lives) Annuity. What this means is that at death the income on a Single Life Annuity stops paying (Unless a guaranteed term is selected, discussed below). With a Joint Life annuity, the income continues paying to the second person until they pass away. Normally No Capital is paid out at the death of the last life and no income payments continue to beneficiaries (Unless a guaranteed term is selected, discussed below). Usually the only effect of adding a 2nd life to an annuity vs a single life is that the income paid out will be the income that is the lowest of a single life annuity between the 2 lives. i.e. If they are both the same age then the income will be that of the woman if one annuitant is male and one is female. If both annuitants are of the same sex, then then the income will be that income the youngest would have received on a single life annuity. I am not aware of a product that currently allows more than 2 lives to be linked to the investment. Some providers will let any 2 people be annuitants on the policy while others will only let spouses share a joint life annuity.

- Guarantee Term Selected. This is an option where you can choose to have the income continue paying to your nominated beneficiaries if you (Single Life) or the surviving annuitant (Joint Life) pass away within the selected guarantee term. The income will continue to pay to your nominated beneficiaries for the remainder of the guarantee term. Guarantee terms can be anything form 5 years to 20 years. As an Example:

- You invest R1m to receive a R6 000 pm income on a Single Life Annuity. You take a 10 year guarantee term with your wife as the beneficiary. You receive income for 2 year (24months) then pass away. Since you have passed away WITHIN the guaranteed term your wife will continue to receive an income for the next 8 years (96 months), then the income stops.

- You make the same investment as above but this time you take out a Joint Life annuity with your wife as the 2nd You unfortunately pass away again due to an unexplained ice-cream and coffee incident. This again happens in the 24th month as above. This time the income continues paying to your wife who dies 9 years later (11 years from the start of the investment), she has died out of the initial 10 year guarantee period thus the income stops and no further income nor capital is paid out.

- Third scenario, you pass away at the same time as the scenario above but your wife this time passes away 12 months after you (3rd year from start of investment & guarantee period). Since there is a 10-year guarantee term on the investment and only 3 years have passed the income will still continue paying for another 7 years to your nominated beneficiaries.

Normally, adding a guaranteed term increases the amount of capital needed to provide the same level of income. The longer the guarantee term the higher the cost. This is not always the case and in certain circumstances adding a guarantee term can actually reduce the amount of capital needed due to the intricacies of re-insurance, but this is not normally the case.

As an example:

It costs R 8 217 more on your initial capital invested to have a 10 year guarantee added to your investment if you want the same monthly income. Alternatively, if your capital available to invest is fixed then your monthly income will be lower on an investment with the guarantee than one without.

- Escalation rate of Income. Your initial Starting income is affected by the annual increase you select on your income payments. If you have a fixed amount of capital to invest, then for the same capital amount invested your starting income will be lower the higher your selected escalation rate. This means that to receive the highest initial income you should choose a 0% escalation. This means you get the highest income in the beginning, but it will NEVER increase for as long as you live which becomes a problem with inflation down the line.

A higher escalation results in a lower initial income for the same capital invested but the longer the investment runs the more income is paid out. Eventually there will be a breakeven point in the future where the escalating income will surpass the non-escalating income.

Example:

Below is a comparison showing the breakeven point on the income of the 2 investments:

You can see that the options you choose with regards to: Guarantee Term, Single or Double Life and Escalation rate affect the initial capital investment needed to provide the same monthly income depending on the structure of the investment OR if you are investing the same amount of capital but make changes to any of the 3 options then the Income you receive will differ for the same capital invested.

With a Guaranteed Life Annuity you have paid an insurer / investment provider to carry the risk of you living longer than your capital would have lasted if you are blessed with a long life as well as the uncertainty of returns in the market. The “price” you pay (more accurately the benefit you give up) is access to your capital / the ability to take chunks of capital as and when you please. As well as the benefit that any capital that is not used up before you pass away is inherited by your dependants.

- Lastly some providers offer a Medical Underwriting Option, where they take your personal health into consideration which leads to a personalised life expectancy. If your life expectancy is lower than the actuarial average, then you can receive an enhancement to your guaranteed income (Income bump or increase) since statistically the provider is expecting to pay for a shorter period of time. If however you out-live their expectation, the benefit is yours and you continue to receive the higher income until you pass away.

- Capital Retention Option. Some providers will give you the option to select a capital amount to be paid out at either at your death or at the death of the 2nd annuitant (usually your spouse) in the case of a Joint Life Annuity. This amount can either be 100% of the invested capital or a lower %. This is done by taking out a life insurance policy on the life of the investor to be paid out at death. BUT the premium from the policy is effectively deducted from the annuity income you get paid and for this reason your normally receive a much lower guaranteed income.

Apart from the Differences & Features discussed above what follows below is a summary of Guaranteed Life Annuities both Voluntary and Compulsory, compared to a Market Related Investment that provides for an income. This can be of a Compulsory Market Related Investment such as an ILLA (Investment Linked Life Annuity) or a Discretionary Market Related Investment. I will not get into comparing the tax differences on Voluntary and Compulsory Investments since both are available in the Guaranteed Investment Space and the Market Related Investment Space.

For the purposes of this discussion we are comparing the features of Guaranteed investments with Market Related Investments and assume in this case that the tax treatment for the 2 are the same (I.e. ILLA vs Compulsory Life Annuity and Discretionary Investment vs Voluntary Life Annuity)

But first what is a Market Related Investment?

The main feature of market related investments is that there is an element of the unknown present in the expected returns of the investment. What this means is that we are not certain by how much our money will grow every year since the markets are volatile. This volatility is usually referred to as market risk. This risk can be managed and lowered by various portfolio management strategies, but it can never be fully eliminated.

We have an excellent recent example. Prior to March 2020 most people would have said that the Money Market investment is risk free and stable. Then suddenly we get hit with Covid Lockdown, Oil Price and Credit downgrade. Suddenly 6 months later the interest rate on cash is 3% lower (a 50% decrease if you were earning 6% before). So, although your capital may not be at risk in a money market fund your return is still at risk.

These unknown risks have knock on effects such as:

Uncertainty of how long your capital will last at the rate that you draw income. This means in a market related investment if you do not manage your income drawdown carefully you could deplete all your capital before you pass-away. This is why so much care goes into income planning and re-planning to constantly be taking account of changes to your investment environment and you need to try make sure your investment doesn’t “die before you do”.

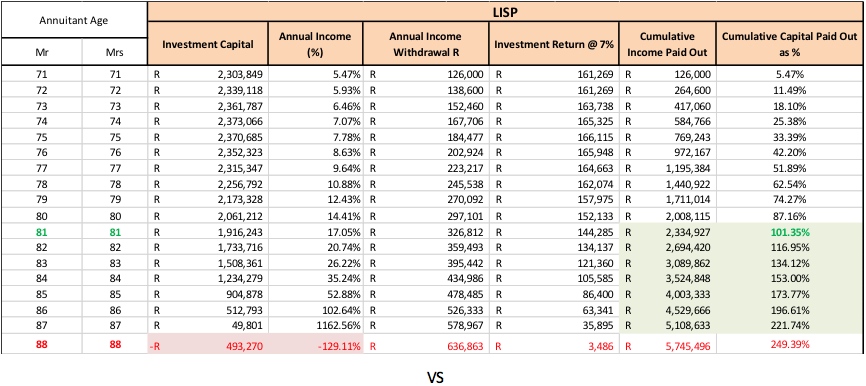

Below is a comparison of the same capital amount being invested R 2 303 849, with the same income taken on a Guaranteed Investment vs a Market Related Investment R 10 500pm (R 126 000 pa) increasing at 10% each year (An investment growth of 7% has been assumed on the discretionary investment (cash +2.5%):

You will immediately notice that with the discretionary investment your capital (and thus your income) will have runout after 17 years. What this means in this particular example, is that if you live longer than 17 years, you would effectively have outlived your capital. The only way to address this with in the Market Related Investment is to:

A: Take more risk. Not advisable for an investor in their 70’s in retirement.

B: Draw less income. Not a pleasant prospect having to cut down on your lifestyle in your “Golden Years”

Alternatively, had you invested in a Guaranteed product you could have happily carried on with an increasing income till 100 years of age if you are to be so lucky. In the above table you can see that after 10 years the total income paid out will have exceeded the initial capital invested.

Ok…. So, what’s the catch? And yes, there is most certainly a catch. If you are invested in the Guaranteed investments and both you and your spouse (the above is a double life annuity) do not survive for a period longer than 10 years from starting the investment then you effectively have ‘lost’ your ‘Leftover’ Capital. (Well not yours but your beneficiaries / Children). Had you been invested in a Market related investment your beneficiaries would inherit any ‘leftover’ capital.

Secondly you also need to consider that lets say in your 3rd year of taking an income. If you had a large unexpected expense such as a large medical bill, you would have the option to withdraw a lumpsum from your Market Related Investment to cover the expense (Yes it would shorten your income period since there is less capital but you would have that option), that option is not available on a Guaranteed Investment.

So, to compare a Guaranteed Income Product VS a Market Related Income Product

Conclusion:

I am not saying one investment option is better than another, but I think it is time to start considering including guaranteed investments into the ‘Income Mix’ since the difference now between low risk cash rates and guaranteed income rates is a lot wider than it was a year ago. Secondly the low growth, low interest rate and uncertain volatile markets make these investments a good option to use to introduce some stability in your income planning.

A specific example where using a guaranteed income can be very useful is in providing for Medical Expenses in Retirement. The problem with Medical Expenses is that they escalate at about 12% pa which is way above the average inflation rate in SA. This creates a problem in retirement especially since medical expenses become a larger part of your budget the older you become. If you have to provide for these expenses out of a market related investment you need to keep increasing your drawdown at a rate higher than inflation and higher than the return you have received on your portfolio (At least over the last 5 years).

This problem could easily be solved by separating enough capital to provide an amount equal to your medical expense need with an annual escalation of between 10% to 15%.

Disclaimer:

This article is of a general nature and for information purposes only and not meant to be construed as advice. Should you require advice, please contact your Certified Financial Planner